Publicly traded Japanese companies face unprecedented pressure to deal with unexpected acquirers knocking on their doors. Brian Yap reports

Seeking to boost competitiveness and growth, Japanese corporates, supported by recent government efforts to encourage takeovers, have been aggressively making strategic acquisitions of publicly traded companies in Japan in the past year.

These developments have triggered unsolicited tender offers, some of them being in the billion-dollar range, that might have drawn public backlash and been shunned by banks and securities firms just over a year ago, senior private practice and in-house lawyers in Japan have told Asia Business Law Journal.

With the recent upshot in unsolicited tender offers, or uninvited takeover bids, to acquire shares from shareholders of listed companies, publicly traded Japanese companies are under unprecedented pressure to prepare for unexpected acquirers knocking on their doors, rather than turning them away with a simple ˇ°noˇ±.

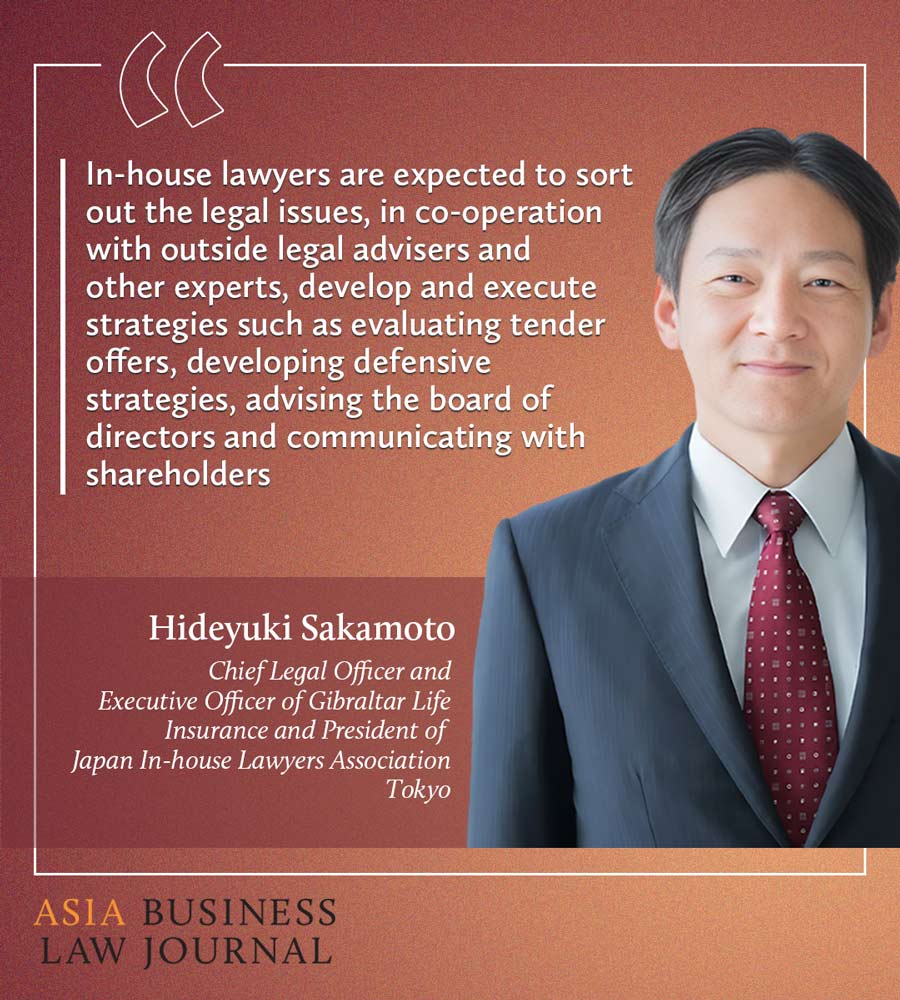

Hideyuki Sakamoto, the chief legal officer and executive officer of Gibraltar Life Insurance in Tokyo, says that such unconsented acquisitions introduce ˇ°unprecedented challengesˇ± to corporate management teams, significantly impacting their businesses and affecting relationships with stakeholders, while entailing intricate legal implications.

ˇ°In-house lawyers are expected to sort out the legal issues in co-operation with outside legal advisers and other experts, and develop and execute strategies such as evaluating tender offers, developing defensive strategies, advising the board of directors and communicating with shareholders,ˇ± says Sakamoto, who is also the current president of the Japan In-house Lawyers Association.

In August last year, JapanˇŻs Ministry of Economy, Trade and Industry (METI) issued guidelines for corporate takeovers following more than nine months of discussion by the Fair Acquisition Study Group and a two-month public consultation.

Under the guidelines, based on results of the discussion among 17 members including lawyers and professors, the target companyˇŻs management or directors should promptly report any acquisition proposal to the board of directors on receiving it. Board directors should give ˇ°sincere considerationˇ± to takeover offers made in good faith.

According to the METI, between 2012 and 2021, Japan recorded 476 tender offer deals in total, and unsolicited ones accounted for 3.8% of them. In comparison, the US saw 16.6% of its 584 tender offer deals being unconsented, while such transactions in the UK made up 19% of 211 acquisitions in the same period. Germany, on the other hand, recorded 9.2% of its 326 tender offer bids as unsolicited, while France witnessed the least number of unsolicited takeovers, accounting for 0.9% of 331 tender offers in total.

Based on research by Asia Business Law Journal, between the start of last year and the end of May this year, at least seven unsolicited tender offers have been publicly announced, launched, completed or withdrawn in Japan. The period under study coincided with the METIˇŻs establishment of the Fair Acquisition Study Group in November 2022, and the release of guidelines for corporate takeovers in August last year.

But, according to Clifford ChanceˇŻs Tokyo-based M&A partner Michihiro Nishi, when factoring in unsolicited takeover bids that have merely been proposed in recent times, the actual figures on unsolicited takeover bids have been ˇ°quite staggeringˇ±.

The growing momentum around unsolicited takeover bids has been fuelled in part by a gradual change of sentiment towards such acquisitions among banks and securities brokers, who have previously been worried about reputational risks.

ˇ°Executing a tender offer in Japan requires appointing a securities firm as an agent, and finding one willing to engage in unsolicited offers used to be a challenge,ˇ± says Nishi. ˇ°Now, with a sound business rationale, many reputable firms are open to advising on such offers, reflecting a significant shift influenced by the new guidelines.ˇ±

Strategic buyers now think they can use the METIˇŻs latest guidelines to justify their intention to launch an unsolicited tender offer bid, and to convince the target companyˇŻs management to accept it. But this doesnˇŻt necessarily mean that companies now have a free hand to go around town gobbling up strategic targets.

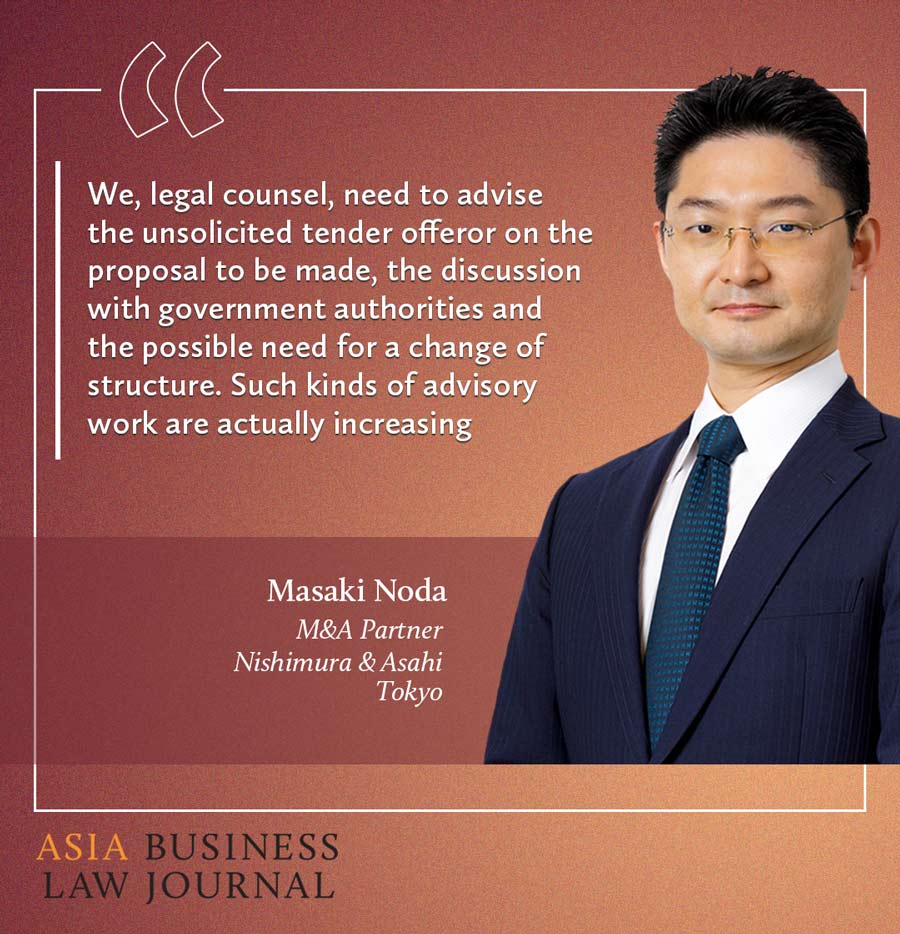

ˇ°We, legal counsel, need to advise the unsolicited tender offeror on the proposal to be made, the discussion with government authorities, and the possible need for a change of structure, says Masaki Noda, an M&A partner at Nishimura & Asahi in Tokyo. ˇ°Such kinds of advisory work are actually increasing.ˇ±

Nishimura, JapanˇŻs largest law firm by headcount, has been mandated as the strategic buyer counsel in some of the largest unsolicited tender offer deals in the past year. One such recent transaction was the Japanese life insurance giant Dai-ichi Life HoldingsˇŻ USD2 billion unsolicited takeover bid for the Japanese employee benefits provider Benefit One from Pasona Group, which closed in March this year.

In December last year, Dai-ichi Life made an unexpected competing takeover bid to acquire the Tokyo Stock Exchange-listed Benefit One from parent Pasona, which had earlier agreed to sell its stake to the medical information website operator, M3. Dai-ichi LifeˇŻs move took many in Japan by surprise, as life insurers have long been considered to be among the most conservative of companies in the country.

But there are many legal issues involved in an unsolicited tender offer, arising from matters including how the acquirer accumulates shares of the target company before the unsolicited tender offer, according to Naoya Shiota, an M&A partner at White & Case in Tokyo.

You must be a

subscribersubscribersubscribersubscriber

to read this content, please

subscribesubscribesubscribesubscribe

today.

For group subscribers, please click here to access.

Interested in group subscription? Please contact us.

ÄăĐčŇŞµÇÂĽČĄ˝âËř±ľÎÄÄÚČݡŁ»¶Óע˛áŐ˺šŁČçąűĎëÔĶÁÔÂżŻËůÓĐÎÄŐÂŁ¬»¶ÓłÉÎŞÎŇĂǵĶ©ÔÄ»áÔ±łÉÎŞÎŇĂǵĶ©ÔÄ»áÔ±ˇŁ

ŇŃÓĐĽŻÍŶ©ÔÄŁ¬żÉµă»÷´Ë´¦ĽĚĐřäŻŔŔˇŁ

Čç¶ÔĽŻÍŶ©ÔĸĐĐËȤŁ¬ÇëÁŞÂçÎŇĂǡŁ