Drawing on personal experience, I recently had the pleasure of delivering some training on deal structuring to junior lawyers in Singapore as part of the Junior Lawyers Professional Certification Programme, developed by the Singapore Academy of Law.

This column discusses why it is important for lawyers to develop a conceptual framework concerning deal structuring and discusses how deal lawyers add value, particularly in the context of technological innovation. Related issues were discussed in a previous column (see China Business Law Journal, volume 10, issue 8: Transactional lawyering).

As the Singapore Academy of Law noted on its website (www.sal.org.sg/jlp), the programme ¡°aims to equip lawyers of less than five years post-qualification experience with practical skills for disputes or corporate practice, as well as impart management skills and reinforce principles of professional ethics¡±.

The website quotes a statement by Singapore Chief Justice Sundaresh Menon, when announcing the programme earlier this year, that its goal is to ¡°set the industry standard for the holistic development of young lawyers, and which will be seen as a trust mark of quality by employers and clients¡±.

Conceptual framework

Developing conceptual frameworks is an important part of professional development for lawyers. They help lawyers to answer the ¡°why¡± question ¨C why are things done a certain way? ¨C in addition to the ¡°what¡± question (what should be done?) and the ¡°how¡± question (how should things be done?). It is a critical component of expertise-creation and the ability of lawyers to advise in a comprehensive and holistic manner.

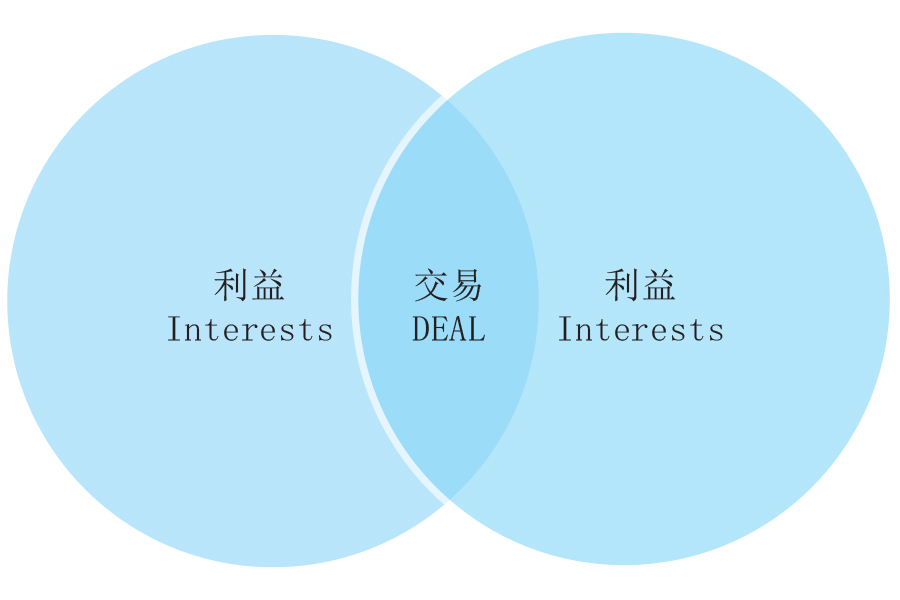

In developing a conceptual framework for deal structuring, it is important to understand the concept of a ¡°deal¡±, the concept of ¡°structure¡±, and why structure matters to a deal. Negotiation theory teaches us that a deal is an arrangement under which two or more people believe that their individual interests can be better advanced through joint action than through unilateral action.

Further, a deal is the space where the interests of two or more parties overlap or intersect (the ¡°deal zone¡±), as depicted in this diagram:

Put simply, structure refers to how the arrangement between the parties is organised. For example, in the context of a transaction to invest in a business, structure involves factors such as the type of deal that the parties adopt (e.g. a share transfer or a business acquisition), the business vehicle that the parties use (e.g. a company or an unincorporated joint venture), and the contractual terms between the parties.

Structure matters for a number of reasons. First, deals are structured in order to reduce the risks about the future and to determine who should bear what risks. Structure is therefore about how risks are identified, managed and allocated between the parties, and the tools that are used for this purpose.

Structure also matters for decision making, particularly in deals that involve a long-term relationship between two or more parties. Key issues in this regard include how parties manage the business (governance), how parties exercise and protect their contractual rights (contract) and how parties resolve any disputes that arise (dispute resolution).

Structure matters in terms of how deals are implemented, and the deal mechanics and processes that are adopted for that purpose. Finally, structure matters in terms of compliance with law.

As noted, deals are structured in order to reduce the risks about the future and to determine who should bear what risks. The relevant categories of risk, and the tools that lawyers use to manage risk, include the following:

- Asymmetric information risk. This is the risk that one party has more, or more accurate, information than the other party and does not disclose all of the relevant risks to the other party. Tools for managing this risk include disclosure and due diligence.

- Counterparty risk. This is the risk that one party does not perform, or may not have the capacity to perform, its obligations as agreed. Tools for managing this risk include information sharing, termination rights (see China Business Law Journal, volume 2, issue 1: When a contract comes to an end) and material adverse change clauses (see China Business Law Journal, volume 7, issue 1: MAC clauses).

- Credit risk. This is the risk that one party will not have the financial capacity to meet its financial obligations, which is particularly important for financiers. Tools for managing this risk include asset security and guarantees.

- Compliance risk. This is the risk that the transaction may not be in compliance with the applicable legal requirements. Tools for managing this risk include legal advice and legal opinions (see China Business Law Journal, volume 4, issue 3: Binding and enforceable; and China Business Law Journal, volume 2, issue 4: Advice or opinion?).

- The risk of incomplete contracts. This is the risk of gaps, ambiguities and missing provisions in contracts, and is usually most acute in long-term contracts where relationship is important and where there may be changes to circumstances (e.g. joint venture agreements and shareholders agreements). The tools for managing this risk include renegotiation clauses and amendment clauses (see China Business Law Journal, volume 3, issue 6: Amend or modify?).

- Exogenous risks. These are risks that arise outside the control of the parties after contract signing, and during the term of the agreement. Tools for managing these risks include force majeure clauses (see China Business Law Journal, volume 8, issue 5: Force majeure).

How deal lawyers add value

In a seminal article published in 1984, in the Yale Law Journal, Professor Ronald Gilson wrote that lawyers function as ¡°transaction cost engineers¡± by devising ways of structuring a transaction to manage and allocate risks, thus making it easier to price the asset (see ). Since then, much has been written about how deal lawyers add value.

This question continues to be relevant today, particularly as technology ¨C commonly referred to as legal technology or legaltech ¨C has emerged to support many of the tools that lawyers use to structure deals. For example, artificial intelligence (AI) is used in the due diligence process to review documents and identify relevant risks; contract automation software is used to generate contracts; and generative AI is used to help lawyers find the law and advise clients on how to comply with the law.

At a ceremony welcoming new lawyers to the Bar in Singapore this year, Chief Justice Menon noted that AI will dramatically impact the practice of law, saying:

¡°Traditionally, junior lawyers have been responsible for basic legal tasks such as document review, analysis and drafting. Indeed, this was one of the primary methods for developing technical competencies and basic lawyering skills.

However, we may soon find that such on-the-job training opportunities are scarce, given the potential of AI to replace lawyers in these tasks. In this evolving landscape, there is a pressing need for us to think of new ways to train and develop our junior lawyers effectively.

One such initiative is the Junior Lawyers Professional Certificate Programme (JLP).¡±

As technology develops to complete much of the work traditionally undertaken by junior lawyers, it is increasingly important for them to receive necessary training to stay one step ahead of technology, adding value to clients and the deals in which they become involved.

Andrew Godwin previously practised as a foreign lawyer in Shanghai (1996 ¨C 2006) before returning to his alma mater, Melbourne Law School in Australia, to teach and research law. Andrew is currently Joint Associate Director of the Corporate Law and Financial Regulation Research Program at the Melbourne Centre for Commercial Law and Honorary Associate Director (Commercial law) of the Asian Law Centre. Andrew has acted as a consultant to a broad range of organisations, regulators and governments in Australia and abroad. He served as Special Counsel and Acting General Counsel of the Australian Law Reform Commission between 2020 and 2024.

")